Mineral Finance 2023: Shifting tides within the mineral industry

Inflation was the centerpiece of both the markets and Main Street in 2022, reaching the highest rates seen in decades.

To combat this inflationary wave, central banks around the world increased interest rates, sparking concerns that a global recession is on the horizon and leading GDP growth projections downward over the course of the year. The International Monetary Fund (IMF) lowering its global economic growth estimates between January 2022 and the start of 2023 from a 4.4% to 3.4% respectively exemplifies the impact inflation has had over the last 12-18 months.

The rapidly changing economic landscape translated to a drop in metal prices and the availability of capital for the mineral sector but exploration expenditures remained strong as the robust financing environment from 2021 carried over into last year’s work plans and programs for most mineral explorers.

Mineral Finance 2023 is broken into the following sections. Click one to jump ahead.

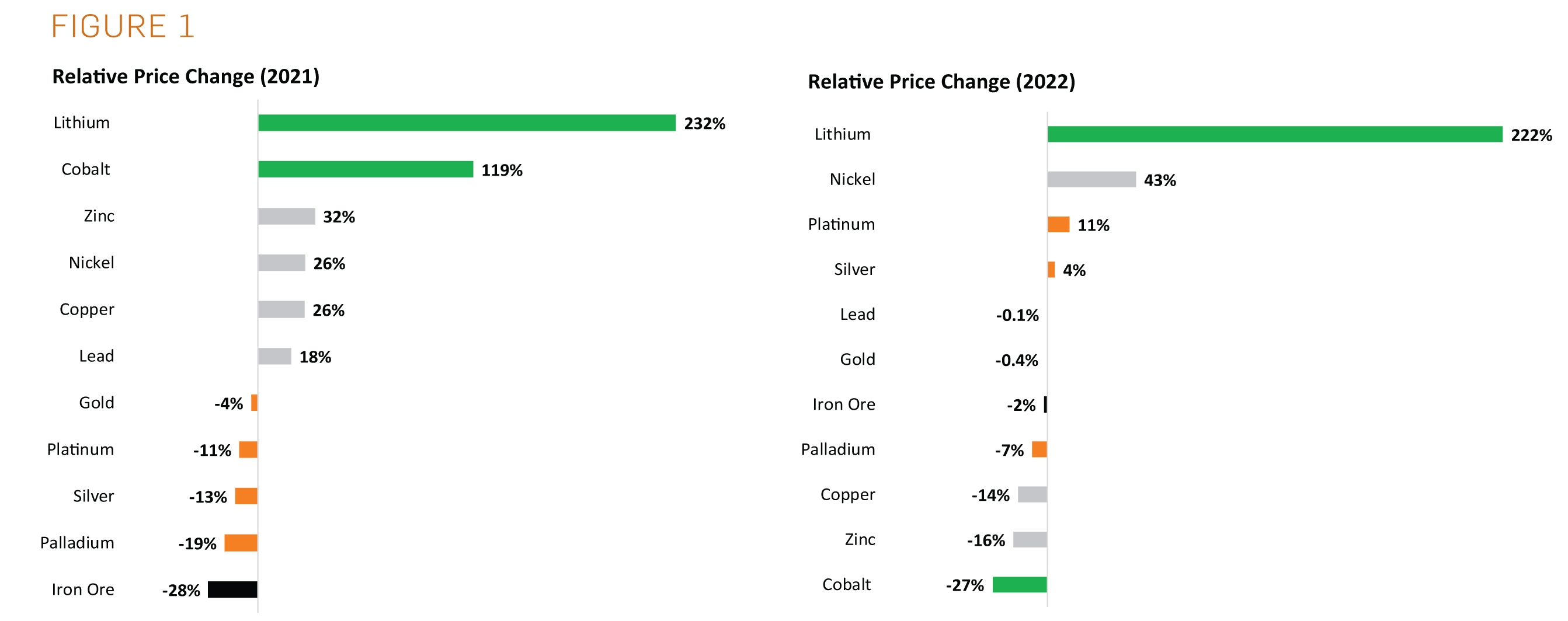

FIGURE 1 presents a comparison of the year-over-year (YOY) price change for a suite in 2021 and 2022.

Comparing the two charts on the right, we see several clear trends:

1) Although up across the board in 2021, base metals were largely under pressure in 2022 - nickel is the outlier and up most likely due to conflict in Europe dislocating supply chains 2) Precious metal prices were a mixed bag in 2022 with platinum and silver showing some modest gains year-over-year, while the gold and palladium price were down for the second year running 3) The two principal battery metals, cobalt and lithium, had prices head in starkly different directions in 2022 with lithium going up multi-fold and cobalt retreating to negative territory.

The decline in most base metal prices likely stems from global economic uncertainty taking hold and a weakening demand for industrial materials implied by growth rates falling below expectations. The decline also likely highlights a switch from an extended period of relatively low interest rates that have prevailed since 2008, to a higher rate environment at least in the near term.

The gold price ended 2022 nearly unchanged from a year prior as recession and inflation fears seem to be tempered by a strong U.S. dollar. Palladium was down over the year, perhaps from recession fears and weakening demand in the automotive market. Platinum led the precious metals group, climbing more than 10% as the market weighs potential supply constraints from Europe due to conflict.

Looking at two of the leading battery metals reveals a stark split in price trajectory. Lithium was the best performing metal for the second year in a row while cobalt dropped from near the top of the chart in 2021 to the bottom in 2022. Cobalt’s price decline seems to have been triggered by electric vehicle (EV) and electronics battery manufacturers signaling a reduction in cobalt use due to social and human rights concerns related with cobalt mining abroad.

Figure 2

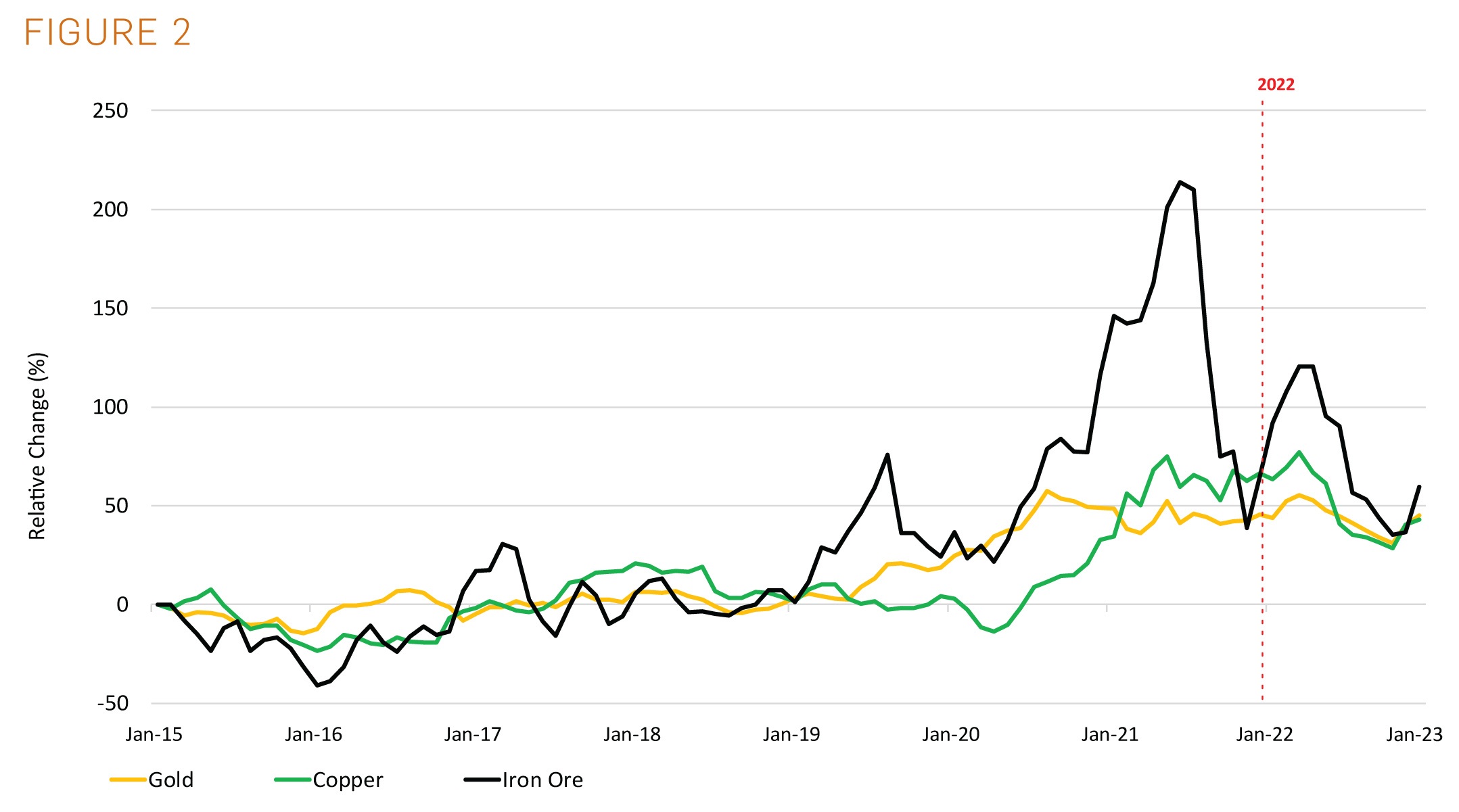

FIGURE 2 shows a multi-year chart for the monthly average price change of gold, copper and iron ore from 2015 onward.

There is certainly some noise in all three metal prices over the time shown. That said, we see a clear bottom in prices in early 2016 and an overall upward trend established from that point until mid-2022, where it seems the growing economic uncertainties and inflationary pressures caused prices to decline. We see very large, short-term spikes in iron ore in 2021 and 2022 as Chinese industrial production began ramping back up post-pandemic. Subsequent COVID lock-downs in 2022 seem to have quenched some near-term demand, driving prices downward into year end.

Figure 3

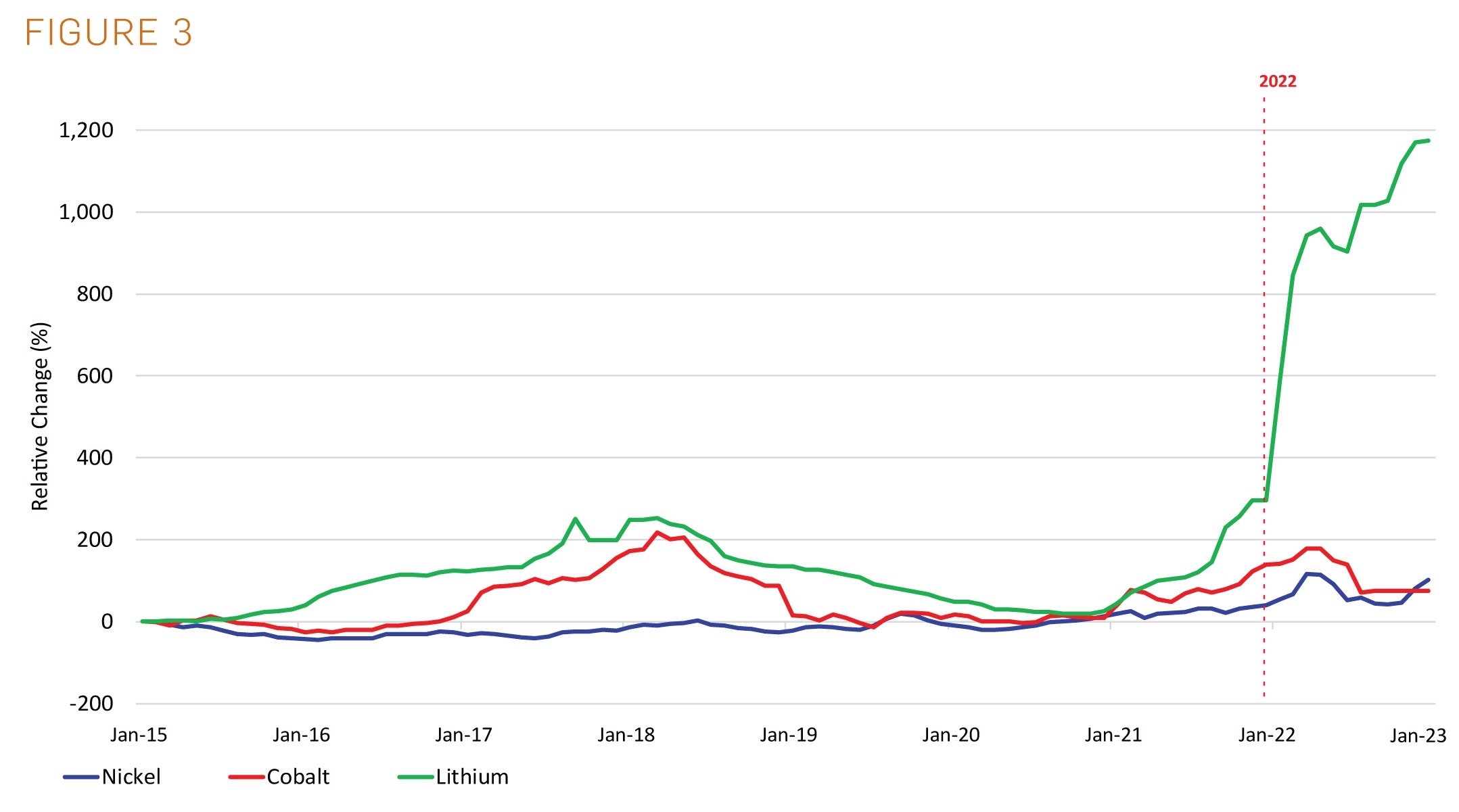

FIGURE 3 presents the long-term price trends of several key battery metals.

Cobalt and lithium prices have moved largely in-step over the last 5+ years but that trend was most definitely broken in 2022 as Figure 3 on the right shows. Note the significant change in the scale of the y-axis from Figure 2 required to plot the climb in lithium over the last 18 months. The divergence that began in 2021 marks a significant split that most likely results from the differing future demand expectations that we noted above.

We can see a much less volatile nickel price over the same period as the metal’s use in batteries still only represents a small portion of annual consumption. The staggering increase in the demand for lithium-ion batteries has not affected the price of nickel in a material way to this point but this could change in the not-too-distant future as new battery tech continue to be developed and refined.

Investment Activity

Figure 4

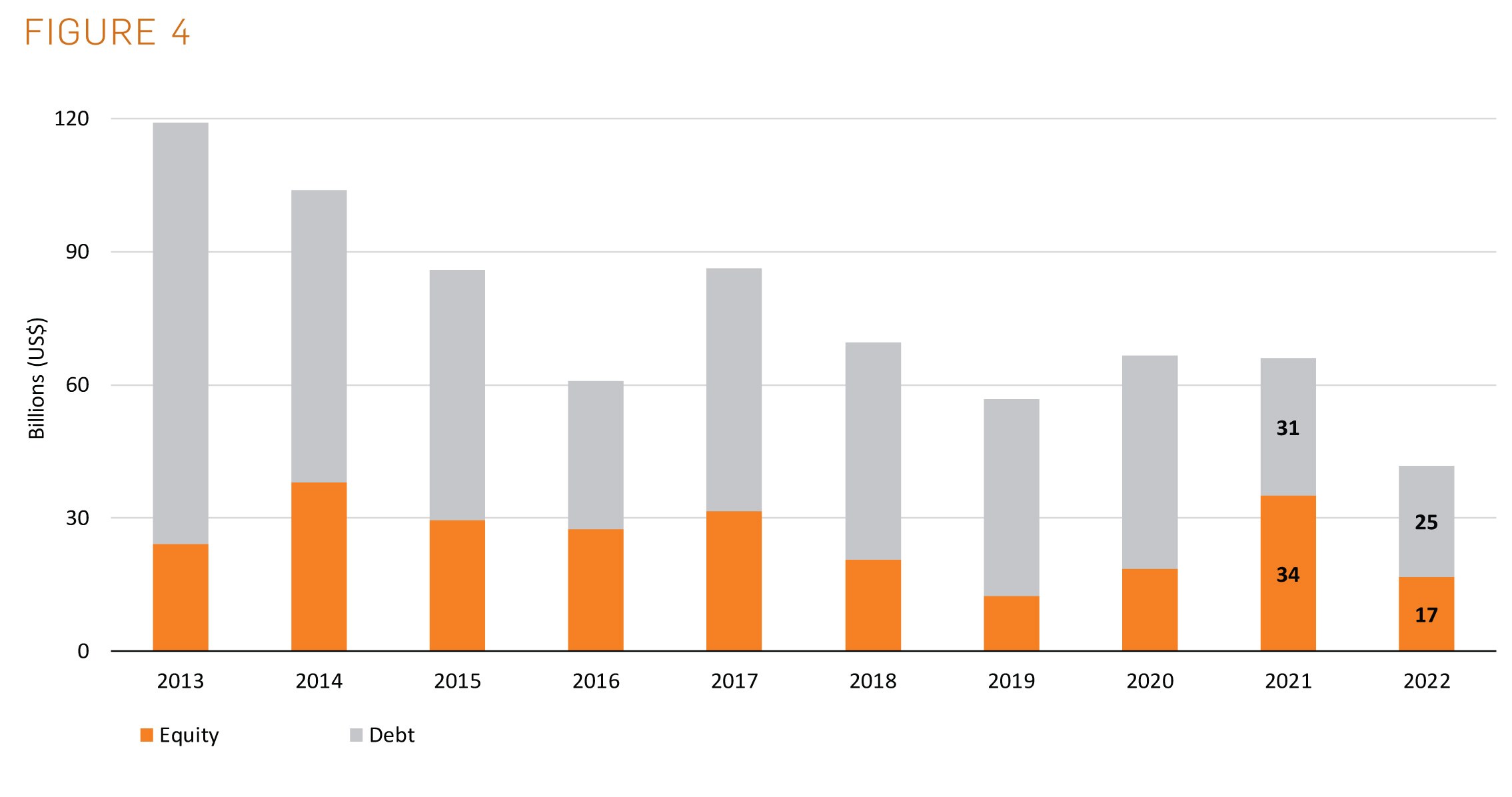

Switching from looking at underlying commodities to fund flows, Figure 4 shows global financing for the mineral sector over the past decade, segmented into equity and debt.

The amount of both equity and debt invested into the mineral industry dropped by a substantial amount in 2022, following along with declining economic conditions and broader market slowdown seen through the year. Debt and equity were down a combined 35% from 2021.

The increase of interest rates by central banks and growing concerns for global economy are likely the key factors behind the decline of availability of both equity and debt capital, as high interest rate and economic uncertainty are expected to reduce the valuations of mining stocks and to discourage companies from issuing new debt.

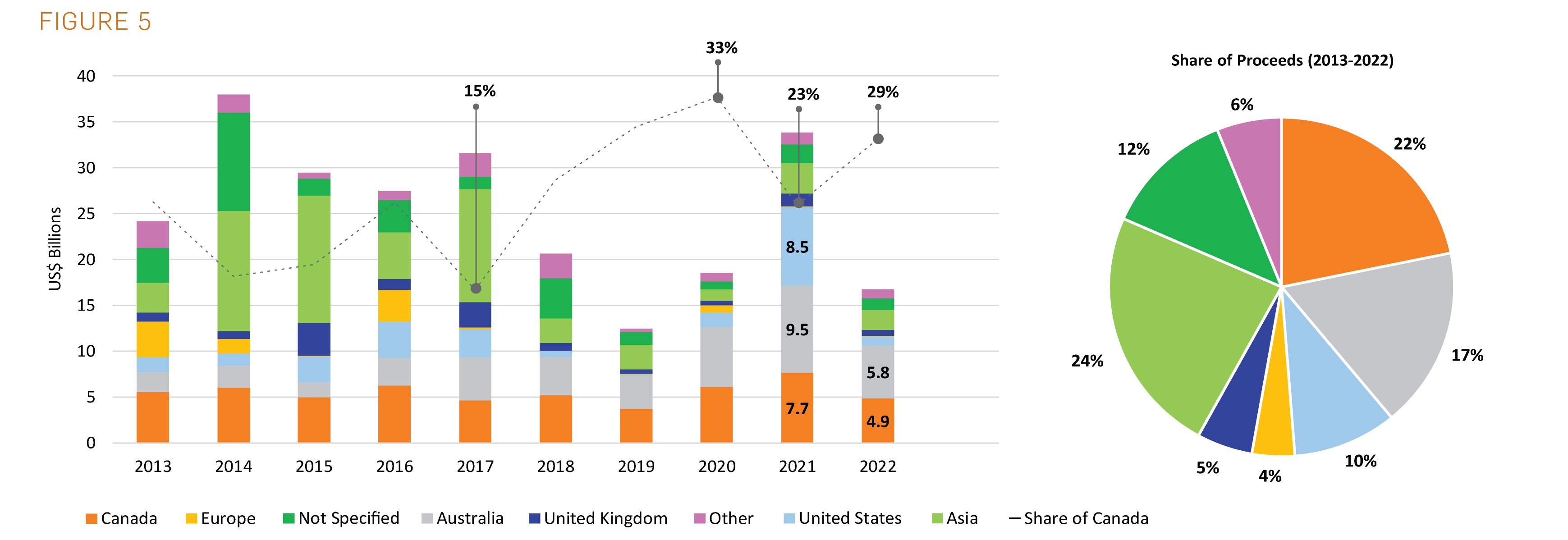

Figure 5

Next, Figure 5 focuses on global equity financing with a breakdown in fundraising by region.

2022 marked a reversal of money flowing into the mineral industry from virtually every global source as equity financing was down 50% from the nearly $35 billion raised in 2021. Australia and Canada continued to lead all other marketplaces for injecting investment into the sector and Canada’s market share increased to nearly 30% (dashed line), which is well above the 10-year average shown in the pie chart on the right-hand side of the figure. At this point, investment into the sector in Canada appears to be holding up as well or better than the other major marketplaces around the world.

The pie chart on the right-hand side of the bar chart shows that Canada has been the top source for raising capital over the last 10 years, accounting for more than 1/5 or 22% of the pie. Although we have seen Australia take the top position in fundraising from Canada since 2020, we observed a more modest slowdown in the Canadian marketplace in 2022. This reflects the depth of our financial service ecosystem’s ability to connect investors to the mineral industry and the effect of targeted exploration incentives provides Canada with an inherent advantage.

An outlier in 2021 and source of a significant part of the global financing drop in 2022 was the United States where funds raised dropped by nearly 90% on US stock exchanges year-over-year. It is noteworthy that roughly 40% of the proceeds (US$3.6 billion) raised in the US in 2021 went into critical minerals and lithium projects and more than 75% of the funds raised can be attributed to only six deals.

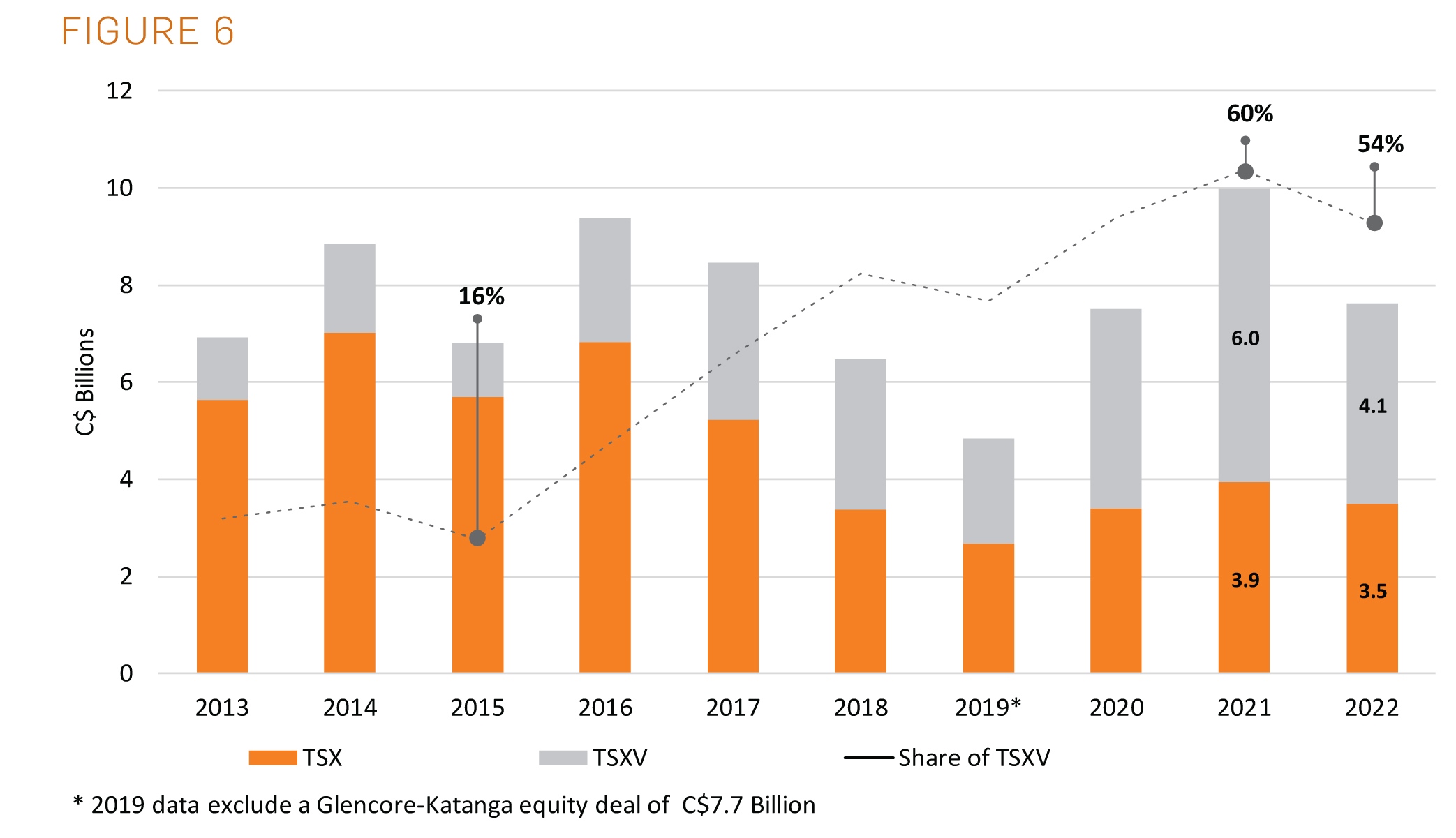

Figure 6

Switching our focus to Canadian markets (and now in Canadian dollars), Figure 6 shows equity raised on the Toronto Stock Exchange (TSX) and the Venture exchange (TSXV) over the last decade.

We saw a healthy rebound in capital investment from all sources over the last couple of years and in 2021 private placements hit a decade high and public offerings and IPOs (see Figure 7 below) were at a level not reached since 2016 and 2017 respectively. Collectively, the amount of money invested into the sector in Canada in 2021 was the most recorded since 2012 and is largely attributable to the upward price trends for most metals recorded over the period and increasing availability of capital.

The same cannot be said for 2022, and as overall markets have weakened, we have seen major indices like the S&P and DOW down as much as 20% or more at points and this has evaporated the amount of risk capital as commodity prices largely trended downward in 2022. On a positive note, while 2022 fell short of 2021’s peak, the amount raised in the year was closer in line with historical averages and well ahead of 2019’s low point.

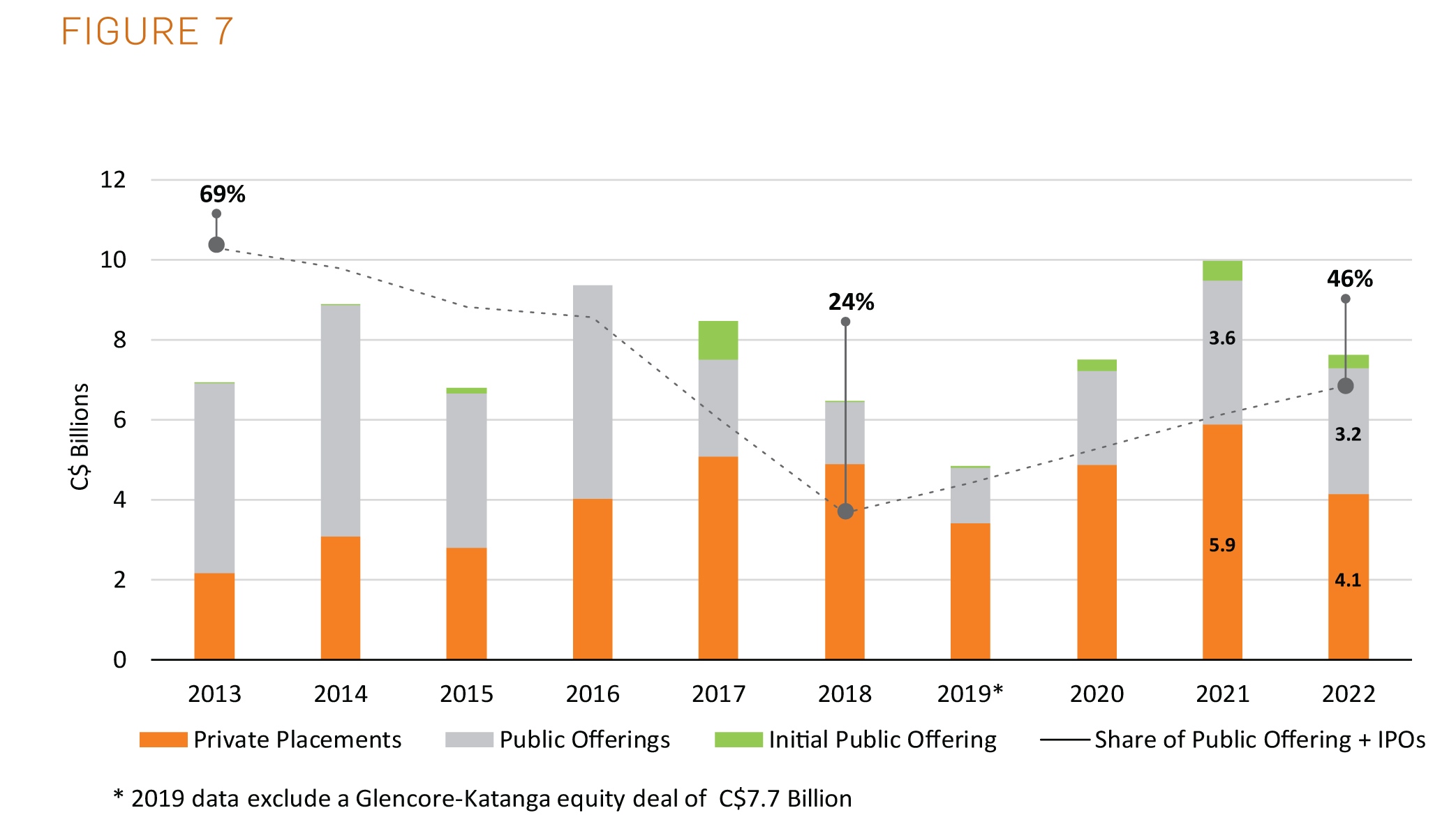

Figure 7

Figure 7 outlines combined financing in TSX & TSXV, disaggregated by the type of equity being issued into the market.

Seeing the share of public deals (public offerings + IPOs) increase over four consecutive years, as the dashed line illustrates, is encouraging as this deal type enables companies to expand their investor base, which typically has positive implications for future fundraising capacity.

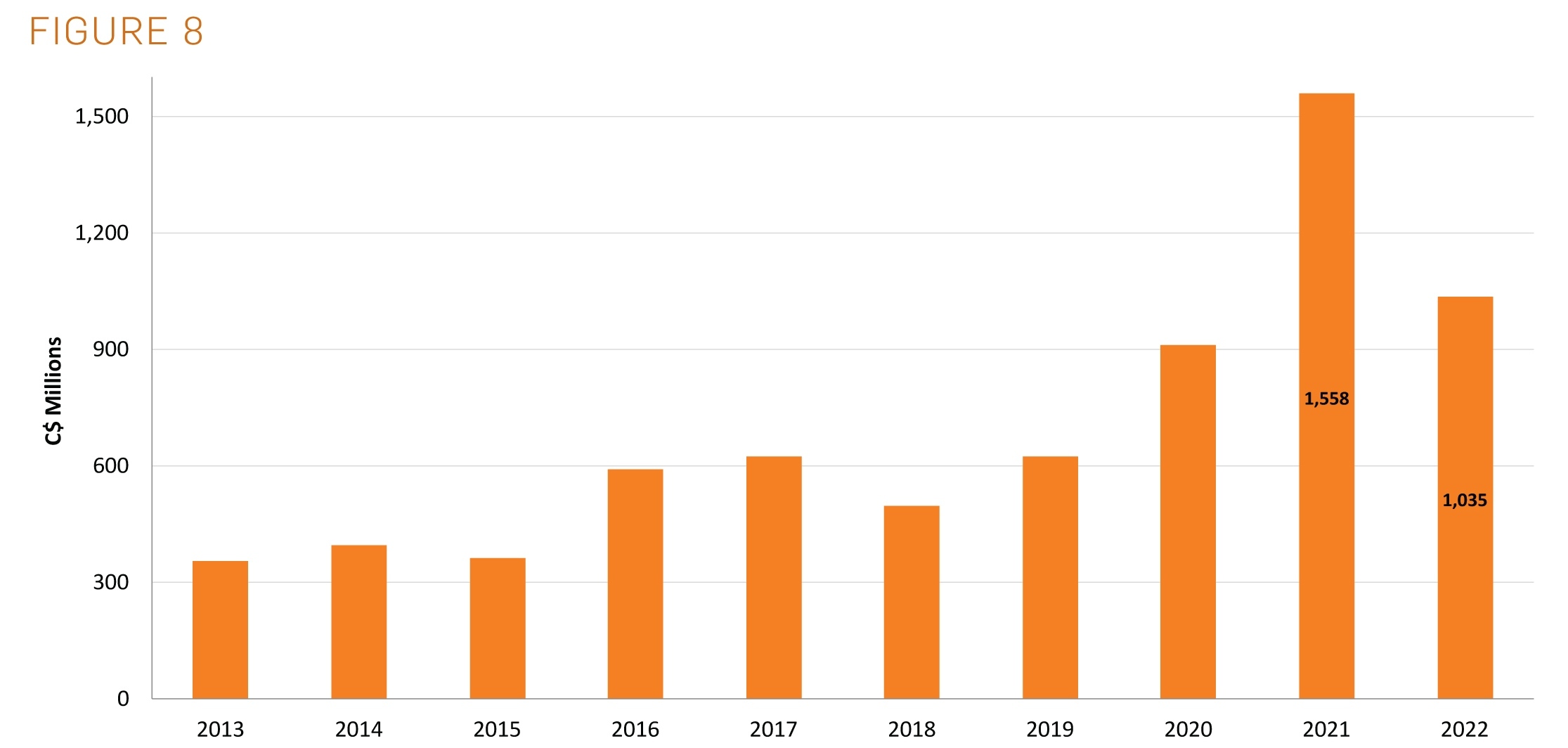

Figure 8

Figure 8 presents flow-through share (FTS) funds raised on Canadian stock exchanges, which must be dedicated towards domestic mineral exploration.

The flow through share regime is a big Canadian advantage and enables Canadian mineral explorers to remain attractive investment in a weak market.

Flow-through has been the source of roughly $2.5 billion in domestic exploration financing over the previous two years and 2021 represented an all-time high. While this peak was not reached in 2022, flow-through financings exceeded $1 billion for only the third time since the regimes inception in the 1970’s.

PDAC’s call to expand available exploration incentives was recognized in Federal Budget 2022 with government committing to a new Critical Minerals Exploration Tax Credit (CMETC) under the FTS regime that will be available until at least 2027. This new incentive represents a roughly $400 million commitment by government and will double the potential tax deduction for investors to 30% for grassroots exploration that targets critical minerals in Canada.

Exploration Activity & Expenditures

The last series of figures (9-12) provides a snapshot of exploration activity, and where investment dollars are being directed on the ground. We start by looking at exploration spending at the global level, then dial down to look at Canadian spending by province and territory as well as by commodity.

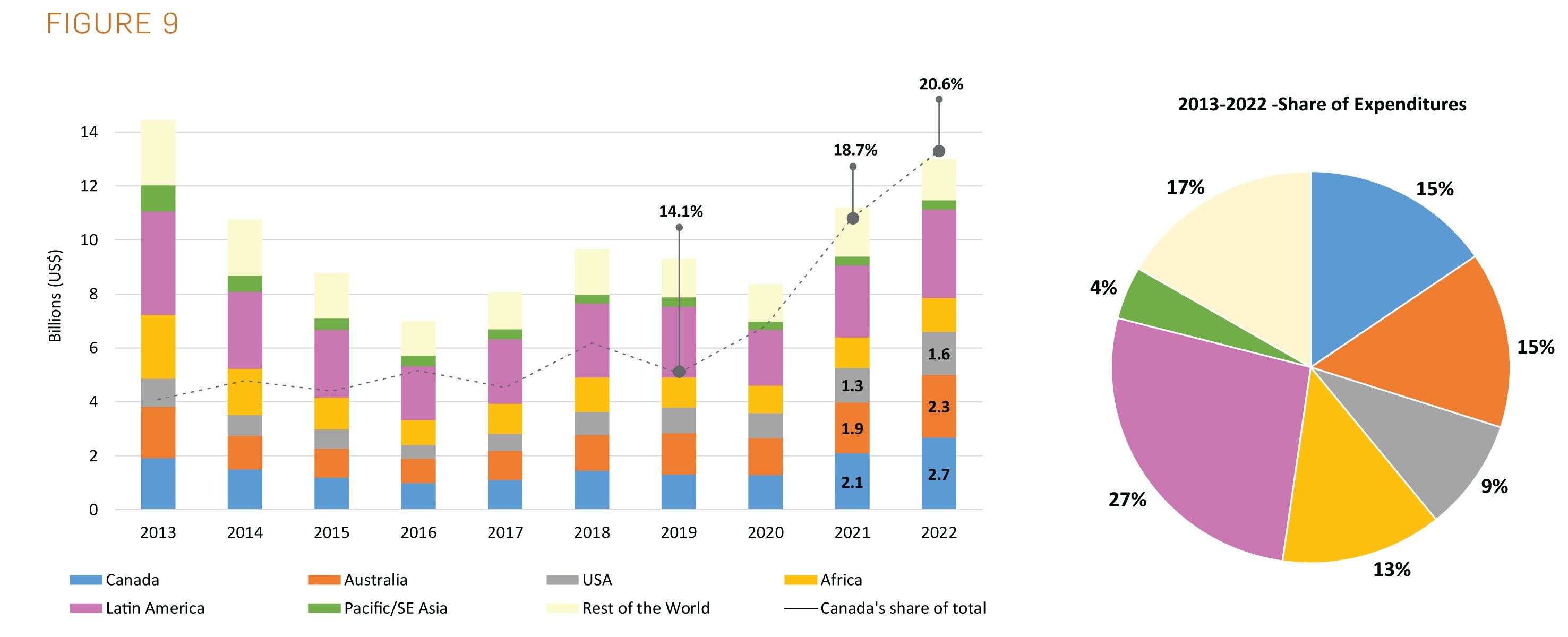

Figure 9

Figure 9 presents global exploration expenditures based on the region where the exploration activity took place.

The figure on the right outlines the amount of mineral exploration dollars going into the ground in various regions around the world over roughly the last decade and we can see that 2022 is likely to represent a relative high point since 2013, both globally and in Canada.

Based on the data from S&P Global Markets, Canada tends to attract more exploration dollars than any other single nation. It is notable that Canada has seen roughly 1/5 or 20% of all global exploration spending over the last two years and if we look at the pie chart on the right-hand side above, it is easy to see how Canada has increased its share of activity relative to the long-term average of ~15%.

Our top position speaks to the highly competitive industry landscape and transparent regulatory processes that exist in Canada, which have been cultivated over decades, and the vast potential for new mineral discoveries that exists from coast to coast to coast.

That said, Australia has closed the gap over the last decade, claiming top spot for mineral exploration spend in both 2019 and 2020, which is a healthy reminder for our regulators and governments that we must work on a continuing basis to bolster Canadian competitiveness, regulatory certainty and ensure we have a vibrant mineral industry for generations to come.

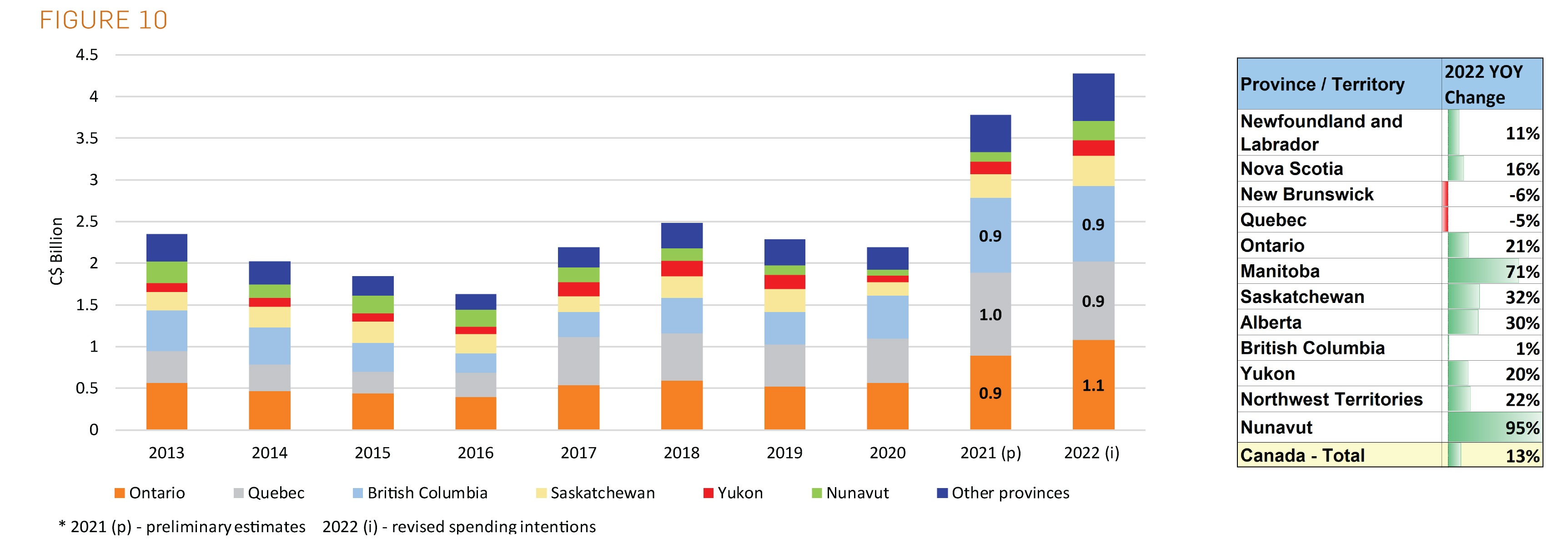

Figure 10

Figure 10 gives a breakdown of the amount exploration spending by region in Canada over the last decade, and similar to the global trend, we see Canada surpassing 2021 to reach a recent high in 2022.

Activity in 2022 established a new all-time record, surpassing the $4.2 billion in domestic exploration spending reached in 2011. Ontario received the highest amount of investment for mineral exploration during the year and it consistently ranks in the top three regions along with Quebec and B.C. These three provinces account for over 70% of the total amount of money going into the ground for mineral exploration in 2022.

It is no surprise to see a high level of exploration activity in Canada in 2022 given the amount of equity raised in the markets in the previous year and the peak in FTS issuance, as we know FTS funding must hit the ground within 12-18 months of those new shares being issued into the marketplace.

With a lag period between financing activity and exploration in mind, there is a good chance we will see an exploration slowdown in 2023 on the back of markets cooling in 2022, both in terms of total amount of equity and flow-through share funds raised.

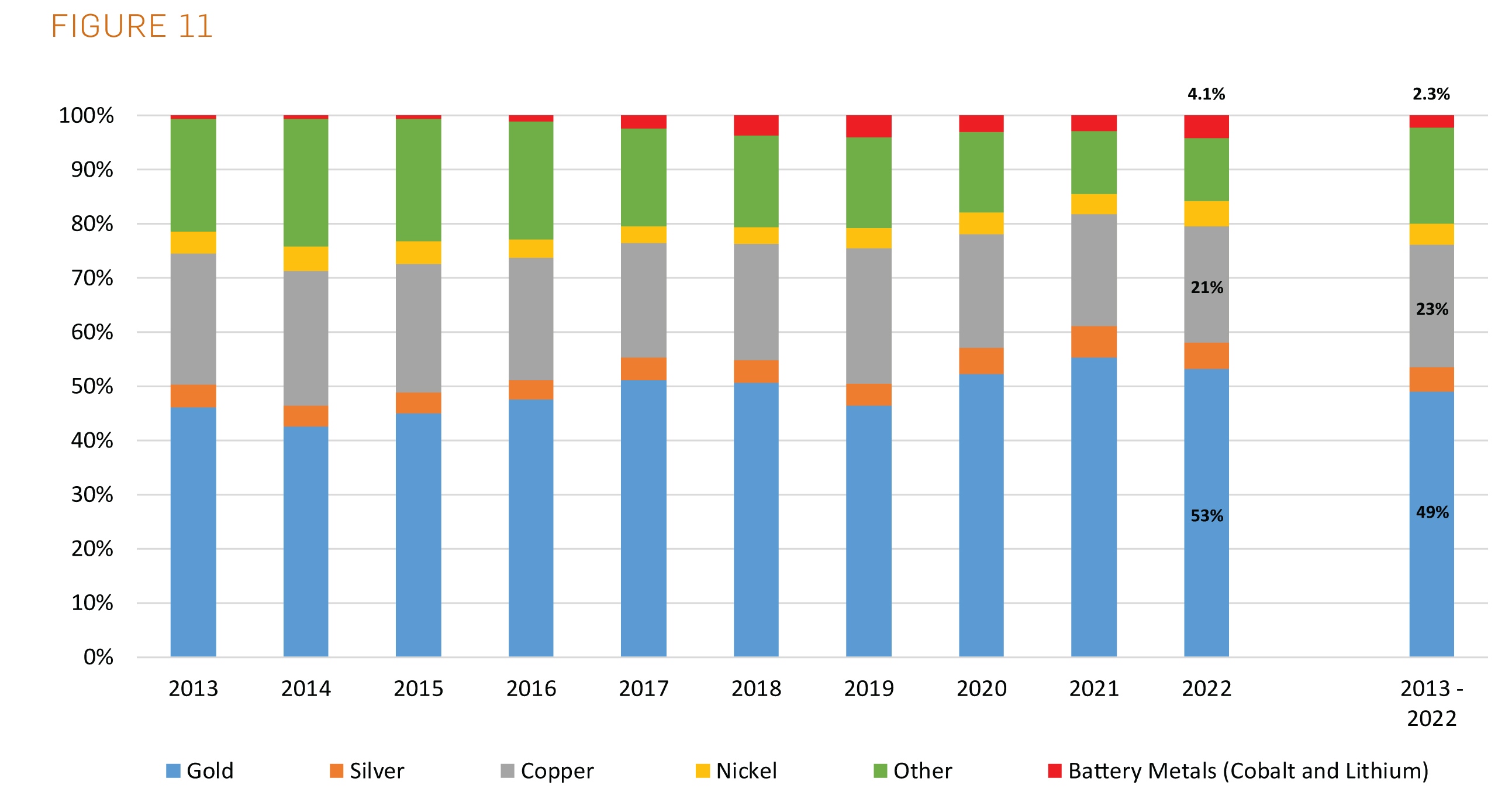

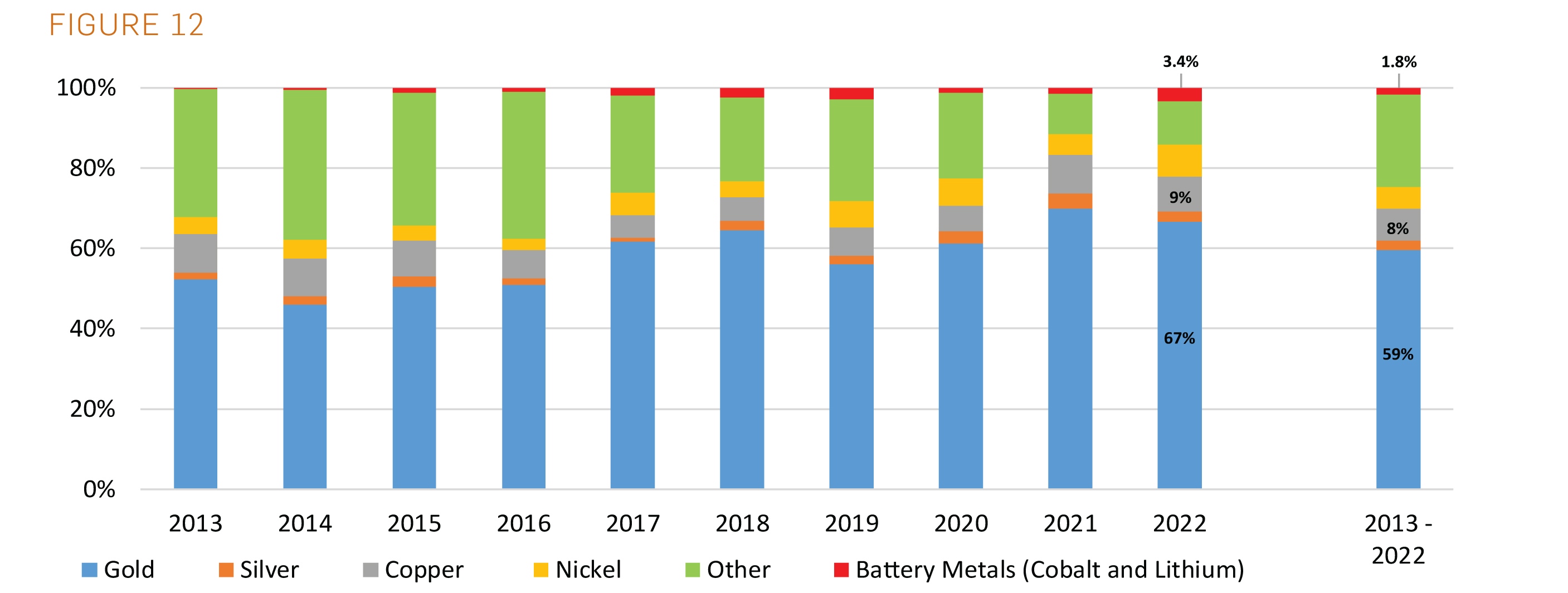

Figures 11 and 12

Figures 11 and 12 compare global and Canadian exploration spending over the last decade, respectively, and differentiate between targeted commodities.

These two figures illustrate the dominance of gold in terms of exploration budgets, with over half of the global spend dedicated to gold exploration, and this share has been increasing throughout the past decade.

With that said, we have begun to notice an interesting trend both globally and in Canada as the amount of funds going towards exploration for battery minerals like lithium, cobalt and graphite is growing. While it is still well below 5%, these critical minerals attracted roughly double the proportion of the global budget in 2022 versus the 10-year average. The proportional growth in critical mineral exploration seems to come in part from a decline in dollars going towards diamonds, uranium and potash.

A comparison of domestic and global budgets reveals that the main difference is a higher share of domestic gold exploration (60% vs. 50%), which is offset by a lower share of copper exploration (8% in Canada vs. 23% globally). This likely reflects a difference in deposit scales, infrastructure availability and the potential for improved economics for copper projects outside Canada when compared to other mining regions such as Chile.

Market activity seems to be off to a bit a slow start in 2023 with a little over $420 million raised on the TSX/TSXV in the month of January, which compares to roughly $620 million and a whopping $1.25 billion raise in the same month in 2021 and 2022 respectively. This could signal a tough year for the mineral industry in accessing new capital, however, we will closely watch the trajectory of major commodity prices like copper and gold to guide whether sector investment will trace up or down from where we left off in 2022.

Sources

Numbers are based on PDAC data sourced from S&P Global Market Intelligence, TMX Group and Natural Resources Canada (NRCan).

Metal Prices (Figures 1-3): S&P Global Market Intelligence

Financing (Figures 4-8): Figures 4-5: S&P Global Market Intelligence Figures 6-8: TMX Group